How to Prioritize Your Money Savings : You’ve covered the necessities like rent, the light bill, and groceries, and now you’ve got some money left over. You know you’re supposed to be saving, but where do you even start? Understanding a few principles can help you prioritize your savings goals and figure out where to put your money.

In this Article Money will describe how to prioritize your savings so read carefully this article.

1. The first principle is to focus on retirement.

The first principle is to focus on Retirement. For most people, retirement is likely to be the biggest financial goal of their lives, so you may want saving and investing to be a major focus. But if there are financial burdens that could jeopardize your retirement savings, removing them is an important priority.

That’s why an emergency fund is the place to start. Unfortunately, most Peoples don’t have enough saved to take care of a surprise $500 expense like an emergency room visit or car repair, let alone something more severe like losing your job. To protect your long-term savings, you can make setting aside three to six months’ of expenses a top priority.

- Build an Emergency Funds

- Get Employer Match

- Pay Off High Interest debt

- Contribute To Retirement Account

- Contribute To Other Tax Advantage Accounts

- Contribute To A Taxable Brokerage Accounts

To figure out how much you need, add up your essential monthly expenses, things like rent, utilities, and groceries. **beat of pause** It may be helpful to keep your emergency fund in a separate savings account that you can access quickly but won’t be tempted to borrow from for day-to-day expenses.

This account can act as a buffer, so you won’t have to pull out the credit card or raid your retirement account when you find yourself in a jam. Once you’ve got an emergency fund, consider shifting your focus to another common retirement savings obstacle high-interest debt.

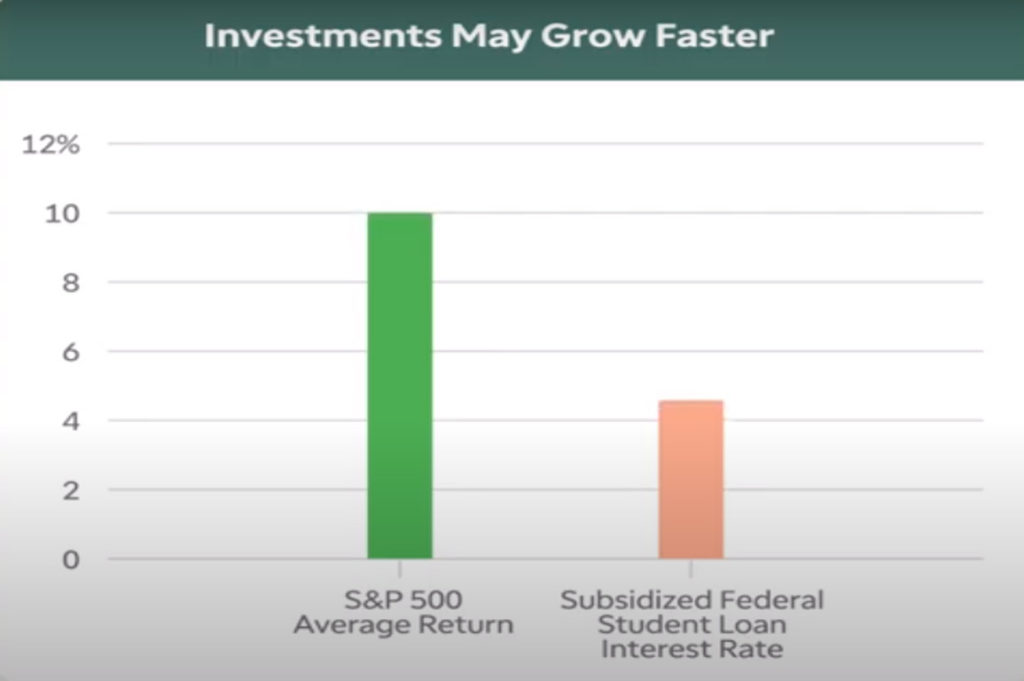

High-interest debt is anything over 5%, so credit cards, personal loans, and especially payday loans. Debt with a high interest rate is likely to grow faster than any money you invest for retirement. Debt that doesn’t reach that 5% threshold, things like most federal Private student loans or mortgages, can be approached a little differently.

It’s important to make regular payments on these, but don’t worry about trying to pay them off early. You’ll likely earn more over the long run by investing than paying off low-interest debt as of 2019, the average annual return of the S&P 500 over the past century is about 10%, much higher than the 4.5% interest rate on a subsidized federal student loan.

Now, it may make sense to put money toward retirement before paying down high-interest debt if your employer matches contributions to a retirement plan, like a 401(k). If your employer offers a match, contribute just enough to get the full amount. You don’t want to pass up free money, so it can be a good idea to prioritize getting that match over paying down debt.

Once you’ve got debt under control, you’re ready to focus even more on retirement. A commonly held rule is to save at least 15% of your income for retirement. So where should you put all that money?

- Focus On Retirements

- Use Tax Advantaged Investments Accounts

- Invest For Long Terms Goals

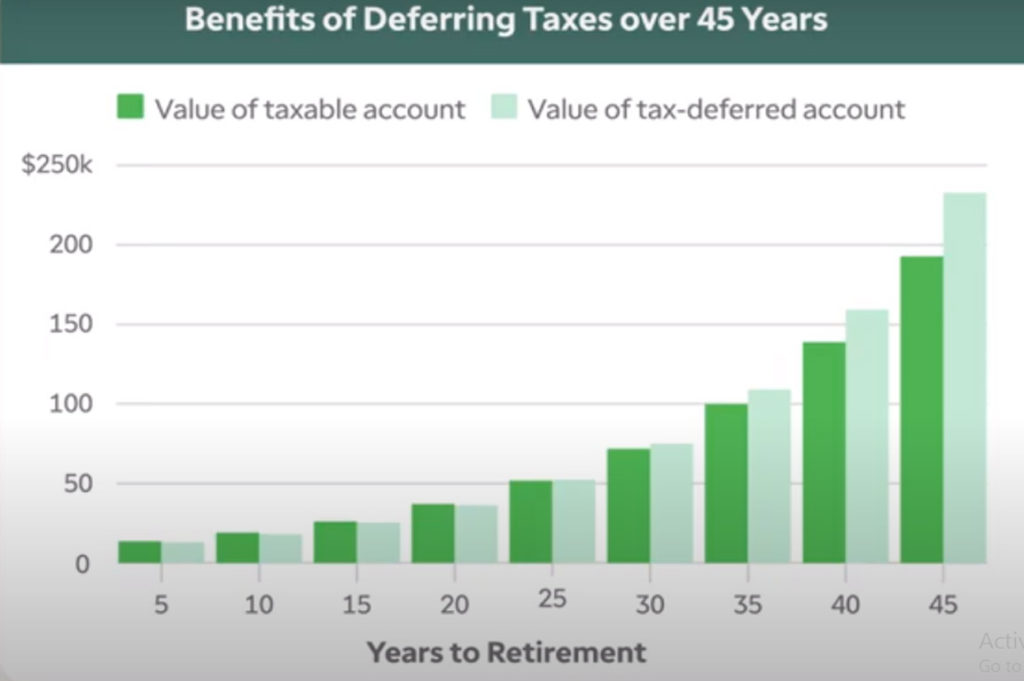

Consider using tax-advantaged investment accounts and minimizing fees to potentially maximize your savings growth. Retirement accounts like 401(k)s and IRAs offer tax benefits that can potentially allow your money to compound more quickly. However, 401(k)s sometimes carry fees that can eat into savings.

If your employer matches, you should still contribute enough to get the full match. But you may want to consider contributing anything beyond that to an IRA, which might have lower fees and more investment choices. After maxing out retirement savings, the next step pretty much depends on your circumstances.

But the same principle applies using tax-advantaged accounts can help to potentially maximize your savings.

For example, if you’re saving for a kid’s college, consider contributing to a 529 plan. It might seem strange that a child’s education is a lower priority than something as far off as retirement, but remember, borrowing for college might be easier than borrowing to fund your golden years.

Health care is another major expense that may require saving. If you’re on a high-deductible health plan, a health savings account is another tax-advantaged account you might want to consider. HSAs are designed to let you set aside and invest un-taxed cash to pay out-of-pocket for medical expenses.

The combination of tax benefits and potential growth from investments may make an HSA an attractive vehicle for saving for medical expenses in retirement. If you’re lucky enough to have maxed out all the tax-advantaged accounts that are available to you, you could also consider money investing for long-term goals in a regular, taxable brokerage account.

A final principle to remember is that investing may not be prudent for short-term goals, like a vacation or a down payment on a house. You may not have time to recover from market downswings, so you might also want to consider using a high-interest bearing savings account rather than investing money you’ll need in the next few years.

If you’ve made it to this point, congratulations you’re a savings pro. The important principles to remember are to focus on retirement, use tax-advantaged investment accounts, and invest for long-term rather than short-term goals. Whatever comes next, make sure you’re keeping the basics well-funded.

Employer Matching Retirement Contributions

Hey guys I’m Money pip this week on mostly money we’re tackling an issue that would make motivational speaker Matt Foley lose his cool people who don’t take advantage of employer matching for the retirement.

Savings also known as people who don’t like free money if the reception thing is the 10 financial Commandments you’d probably find the following items on that list don’t spend more than you earn.

Make your savings automatic and never carry a balance on your credit card but another one that deserves to be on that list is this if your company offers to match your savings to a retirement plan take full advantage of it.

Because it’s basically free money here’s how these plans work if they are offered by your company they will generally tell you that for every dollar or Rupees.

You contribute to your retirement savings they will offer to match it up to certain limits as an example they might say they will match at 50% all your savings up to a maximum of 4 percent of your salary that means that if you were earning $50,000.

you could say 4 percent of that or $2,000 that would be eligible for matching contributions from your employer of $1000 now some companies will match dollar for dollar or 100 percent as another example.

Let’s say your company will match 100 percent of your contributions up to 4 percent of your salary again assuming you earn $50,000 that means you could contribute 2,000 dollars per year into this plan and your employer.

Would kick in an extra $2,000 per year as well now let’s assume you’re 25 and you get a 2 percent raise per year and the rate of return on your investments is 5 percent.

When you turn 65 your retirement portfolio would be roughly seven hundred and twenty thousand dollars half of which was because of your employers contributions in other words in this simple example.

The employer matching program was responsible for three hundred and sixty thousand dollars of your nest egg all you had to do was get off your butt and sign up for it okay I’m gonna leave you with some final thoughts.

If you’re not a personal finance nerd then all you really need to know is you should likely be taking full advantage of any employer matching programs that work for retirement savings.

If you are a personal finance nerd I’m gonna leave some links in the another article down below to further discussion and spreadsheets on this topic keep in mind you have to be on the money pip blog in order to see the description as always if you have any questions or you want to chime in with your own tips please leave them in the comment section down below and thanks.

Thanks for Reading this article . If you’re a smart investor looking to get smarter, stay up to date on new article by bookmarks, follow me on my Facebook page ,and don’t forget to follow Money Pip Instagram Page.

Disclaimer: The views and investment tips expressed by investment experts on https://moneypip.com/ are their own, and not that of the website or its management. https://moneypip.com/ advises users to check with certified experts before taking any investment decisions.